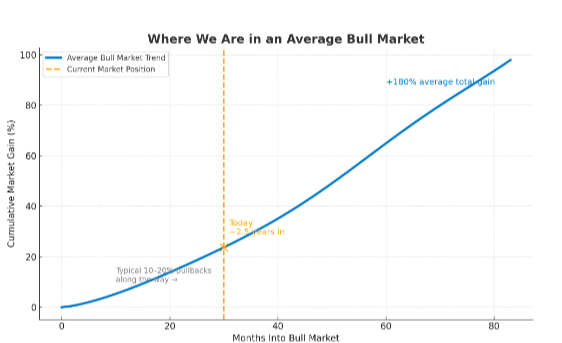

The Big Picture – Average Bull Market

Key stats:

- 🕒 Average Length: 5.8 years (70 months)

- 📈 Average Total Gain: +180%

- 📉 Average Declines During Bull Markets: 3–4 dips of 10–20%

➡️ Current bull market: Year 2½ — roughly halfway through the average!

What Feels Like a Setback Is Just a Pause

A 15% drop only erases a small part of a 180% total bull market gain.

In other words, it is just a coffee break in a multi-year marathon.

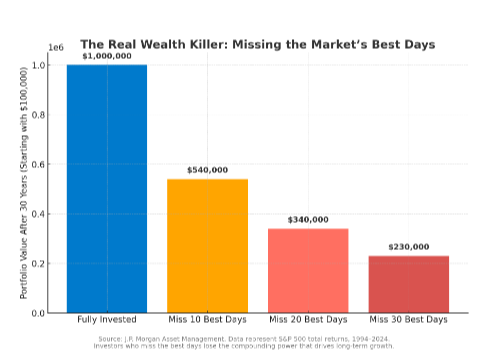

The Real Wealth Killer

- Investor A: Stays invested, capturing every +1%, +2%, +5% gain.

- Investor B: Misses the 10 best days of the decade by “waiting for clarity.”

You need every positive percentage point the market gives you — miss a few, and compounding breaks.

Key Takeaway

✅ Markets reward patience, not perfection.

- Every 10–20% decline is a normal detour on the path to long-term growth.

- Staying invested smooths the ride and captures the compounding effect.

- Hedging or bailing early may feel safe but often costs you the real reward — time in the market.

You don’t need to predict the next downturn — you need to participate in the next recovery. To grasp the urgency of this discipline, read Nick Murray’s blunt words explaining why we must hold and compound the stocks of great companies, uninterrupted:

“Only a couple of generations ago—well within living memory—Dad retired at 65 and died at 73. Mom went to live with the kids. And that was that. Their retirement income came from the government, the union, or the company pension plan—certainly not from their accumulated wealth. It may have made some sense, given that life experience, to just park whatever savings they had at retirement in bonds and CDs, and wait for the end.

Fast forward to today. The commonplace in our time is the two-person three-decade retirement. And beyond Social Security, most people will derive the great preponderance of their retirement income from what they themselves have saved in qualified retirement plans and on their own. This presents an entirely different challenge. Simply stated: it is to keep one's income rising at a greater rate than inflation destroys the purchasing power of that income. Because if history and logic are any guide, an essentially fixed-income strategy over three decades of rising living costs is planned suicide.

The hundred-year inflation rate in the United States is three percent. Compound. At that rate the general cost of living will go up about two and a half times over three decades. If you're fighting that battle with a fixed income, you're going to lose. The only real issues are how badly you lose and how soon.

And even that assumes you actually experience trendline CPI inflation. There is mounting evidence that seniors don't, and won't—if only because healthcare costs are rising at a significant premium to the CPI.

Mainstream equities, on the other hand….have over the same hundred years compounded at more than three times the CPI inflation rate. More directly to the point, they have thrown off cash dividends that have since 1950 been increasing at a rate approaching twice that of CPI inflation.

That's safety, by any sane definition. Because at this point we can forget about “longevity risk;” it has long since become longevity reality.”

From “Target Date Funds: The Fatal Misperception” Nick Murray October 2025

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.

Securities offered through LPL Financial, Member FINRA/SIPC. Investment advice offered through Western Wealth Management LLC , a registered investment advisor. Western Wealth Management LLC and Kennebec Wealth Management LLC are separate entities from LPL Financial.